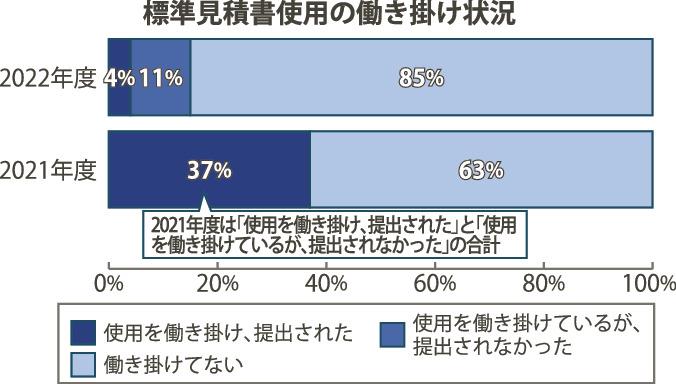

At the construction site level, the use of standard quotations that clearly state the details of statutory welfare expenses is not widespread. In a fiscal 2022 monitoring survey conducted by the Ministry of Land, Infrastructure, Transport and Tourism, in which managers of prime contractors' branches and sites were directly interviewed about the actual state of transactions, only 15% of prime contractors encouraged subcontractors to use standard quotations. Both figures from the survey on subcontracting transactions, etc., targeting individual companies (69.3% in fiscal 2010) and the figures from the previous fiscal year's monitoring survey (37%), which targeted prime contractors of relatively large companies, are both lower. The Ministry of Land, Infrastructure, Transport and Tourism sent a letter to the surveyed companies requesting improvements.

The Ministry of Land, Infrastructure, Transport and Tourism has continued to conduct monitoring surveys since October 2021. In FY2009, we visited 80 locations (including multiple branches and sites for one company), mainly for prime contractors with a completed construction value of 100 billion yen or more. , We asked about the status of subcontracting transactions, passing on prices, and setting the construction period, mainly for construction work with a construction period of about 1 to 3 years and a construction cost of about 1 to 5 billion yen.

A Ministry of Land, Infrastructure, Transport and Tourism official said that the reason for the lack of use of standard quotations was that "Compared to the previous fiscal year, the size of the companies we interviewed were smaller, so the responses may have slowed down." Even within the same company, there are cases in which the responses differ depending on the branch office and site.

The Ministry of Land, Infrastructure, Transport and Tourism strongly advocates the need to utilize standard estimates in order to record appropriate statutory welfare expenses based on clear calculation grounds. Regardless of whether standard quotations were used or not, 92% of the quotations clearly stated the statutory welfare expenses, but there were also cases where the prime contractor did not check whether the amounts were appropriate. .

In order to confirm that the final appropriate amount is recorded, it is necessary to clearly state the statutory welfare expenses in the contract, but the ratio was only 74%. 14% of contracts (14% in the previous fiscal year) have a remarkably low ratio of statutory welfare expenses to the contract amount, and 9% (26%) of contracts have large lump-sum discounts that do not seem like rounding.

In about 30% of cases where such inappropriate handling was suspected, the construction system ledger and other documents were not sufficiently prepared and the authenticity of the content was not fully confirmed.